Skip to main content

menu

Home

About Us

Strategy

Useful Information

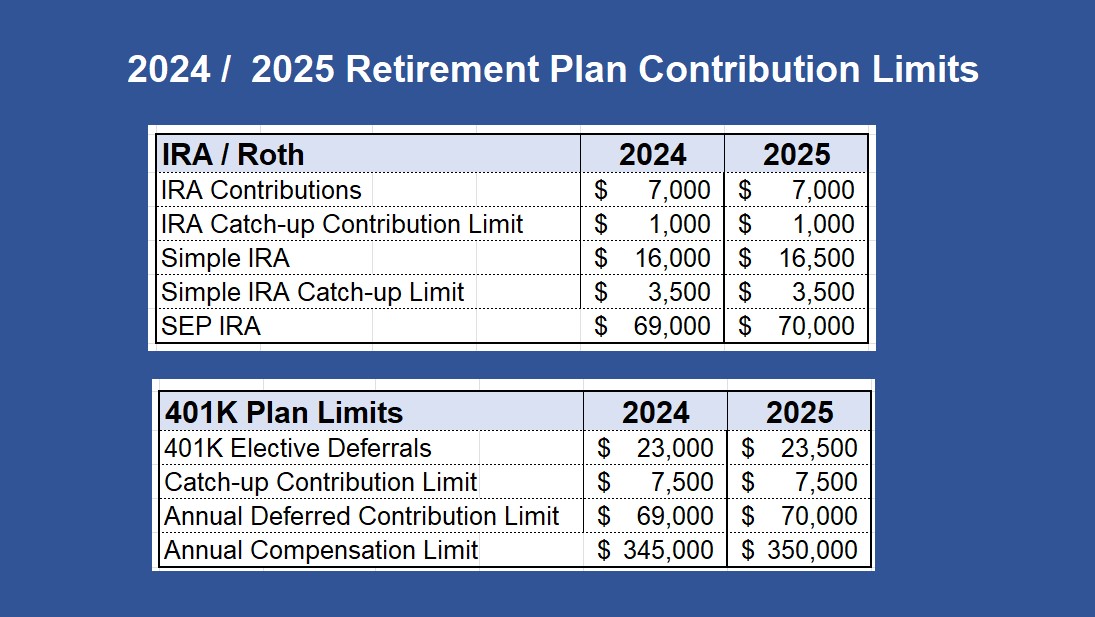

Annual Retirement Plan Limits

Federal Income Tax Rates

Capital Gains Taxes

Estate & Gift Tax Exclusion

Roth IRA’s

IRA

Newsletters

Contact

Client Login

Annual Retirement Plan Limits

© 2026 Lowell Road Asset Management. All rights reserved.