What is an Roth IRA?

A Roth IRA is a type of Individual Retirement Account that was created in the Taxpayer Relief Act of 1997. A Roth IRA is a special tax-advantaged individual retirement account which gives you the opportunity to invest after tax dollars and your investments grow tax deferred and are then distributed tax-free during retirement.

One of the key factors in deciding between a Roth IRA and a traditional IRA is whether to take advantage of immediate tax benefits (traditional IRA) or tax-free withdrawals during retirement. If you believe your income will be significantly lower when older, then a traditional IRA could make more sense. If you believe you will be in a higher tax bracket later in life, then a Roth IRA could be best. A Roth IRA is a powerful investment vehicle when there is a long span of time for earnings to compound and properly invested. According to the Investment Company Institute, more than 1/3 of IRA investors have Roth IRA accounts.

Who can contribute to a Roth IRA?

- Anyone with earned income.

- To be eligible, there are income limitations.

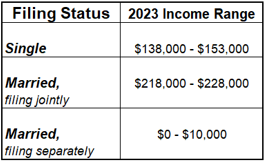

- Single filers cannot contribute if they earn more than $153,000 in 2023 (maximum contribution reduces at $138,000 in 2023).

- Married couples filing jointly, the limit is $228,000 in 2023 (max contribution reduces at $218,000).

Roth IRA Phase-Out Ranges

- If your income doesn’t qualify and you are still interested in having a Roth IRA, a Roth Conversion is an option.

Annual IRA and Roth IRA Contribution Limits

Advantages of a Roth IRA

- Contributions and potential investment gains accumulate tax-free.

- No Contribution age restriction.

- Qualified tax-free withdrawals.

- No mandatory withdrawals (RMD’s)

- No income taxes for Inherited Roth IRAs.

When can you contribute?

You can make a Roth IRA contribution beginning on January 1st of the contribution year until the Tax Day of the following year. This is typically April 15th. For a 2023 contribution, the last day to make a contribution is April 15, 2024.

When can the money be withdrawn?

Beginning at age 59.5, people who’ve held their Roth IRA accounts for at least 5 years can begin withdrawing contributions and earnings without taxes or penalties. An early withdrawal of your contribution can be made anytime since taxes were paid on that amount. Simply put, it would be reversing a contribution. Although early withdrawal of earnings would result in taxes and penalties.

Does a Roth IRA require an RMD? How is an Inherited Roth IRA handled?

Roth IRAs do not require withdrawals or RMDs until the death of the owner. A spouse can then roll that account into their own Roth IRA. A non-spouse beneficiary has 10 years to withdraw all proceeds from an inherited Roth IRA.

What is the Roth IRA Early Withdrawal Penalty?

The Roth IRA early withdrawal penalty of 10% will be applied to the entire distribution when withdrawing contributions before age 59.5. If you withdraw funds without holding a Roth IRA for more than 5 years, you may be subject to taxes.

Exceptions to 10% penalty for early withdrawal

There are certain situations that allow you withdraw money from your Roth IRA without the 10% penalty. You would still be required to pay income tax on the withdrawals. Listed below are the exceptions:

- A first-time home purchase ($10,000 lifetime maximum).

- Qualifying education expenses.

- Expenses related to birth or adoption ($5,000).

- The Roth IRA holder passes away or becomes disabled.

- The unreimbursed medical expenses or health insurance during a period of unemployment.

Roth IRAs are valuable investment tools for retirement savings and tax-advantages. Should you have any questions regarding Roth IRA’s or any other retirement planning questions, please give Lowell Road Asset Management a call.